What to Expect in the Real Estate Market in 2026 – And How Land Investors Keep Winning

What to Expect in the Real Estate Market in 2026 — And How Land Investors Keep Winning

By Jack

If you’ve been watching the housing market and thinking, “Everything feels… stuck,” you’re not imagining it. A lot of the headline numbers look flat. Median listing prices have barely moved overall, and depending on the week you check, it can feel like the market is drifting sideways.

But “flat” is a surface-level description of something much more interesting underneath. What’s really happening is that many markets are going through a reset. Some areas that were absolutely nuts during the post-2020 run-up are cooling back down toward reality. Others are still strong, just not as explosive. And a handful of places are still climbing because demand is relentless and the right kind of inventory is scarce.

That’s why you can look at the big picture and see a small year-over-year change, while your local market feels completely different depending on the zip code and price point you’re watching.

Inventory trends tell the same story. If you track listings over the year, you’ll notice periods where active inventory looks meaningfully higher than last year, and then that gap shrinks—especially late in the year when sellers pull listings, buyers pause, and the whole market gets seasonal. None of that changes the real issue: in most places, there’s still a shortage of the kind of housing people actually want and can actually afford.

And that brings us to the drivers that will matter most in 2026.

The biggest one is still supply and demand—except it’s not just “supply” in general. There is no shortage of luxury inventory in many markets. The shortage is at the affordable end. It’s the $132,000 to $332,000 type of house in some areas, or the equivalent “normal buyer” range in higher-cost markets. That’s where demand lives. That’s where families are trying to buy. That’s where first-time buyers are trying to enter. That’s where builders wish they had more product to sell.

Construction costs don’t help. Materials have stayed elevated. Labor isn’t getting cheaper. Insurance has become a real problem in areas dealing with natural disasters and rising risk—whether that’s hurricanes, wildfires, flooding, or simply the way carriers are repricing exposure. When insurance goes up, carrying costs go up. When carrying costs go up, buying power goes down. That squeezes the end buyer, which squeezes the builder, which affects what the builder can pay for the lots we’re selling into the machine.

Then there’s the rate-lock effect, which is one of the most underrated reasons the market behaves “weird” right now. A massive number of homeowners are sitting on mortgages below 3%. When current rates are materially higher, people don’t move unless they have to. Even if they want to, the payment difference can be brutal. That reduces turnover. It keeps inventory from flowing normally. It creates a strange kind of stagnant demand—not because people don’t want homes, but because they refuse to give up the deal they already have.

Zoning and regulation continue to put their thumb on the scale too. This isn’t a temporary issue. There are always more rules, more approvals, and more friction. In some parts of the country you can still buy a piece of land, put a mobile home on it, and live your life. In many places, that gets harder every year. The result is predictable: it’s harder to build, slower to build, and more expensive to build—which circles right back to the supply shortage at the affordable end.

Add in stagnant wage growth relative to prices and you get a market where affordability is strained, inventory is mismatched, and the path forward depends on what happens with rates.

So what do I actually expect in 2026?

I expect mortgage rates to continue easing from the highs we saw. When rates come down, buying power increases. That tends to push prices up a bit in markets with real demand, because more buyers can qualify and more buyers can compete. It doesn’t fix supply overnight, but it does loosen the gears. It also changes behavior—some homeowners will finally move, some buyers who’ve been waiting will finally act, and the “stuck” feeling starts to shift.

But here’s the part that matters to us as investors: none of this changes the core strategy that works in almost any environment.

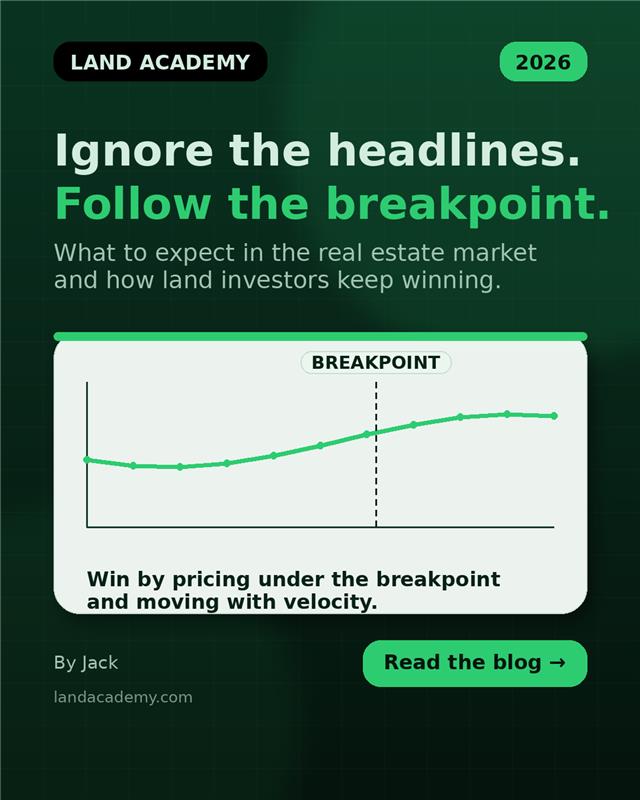

In 2026, your job is to control cheap houses or land in high-demand markets—specifically below the breakpoint.

That breakpoint concept is everything. In every market, there’s a price point where demand accelerates. It’s where buyers can afford the property, where the property looks like a bargain compared to everything else, and where listings tend to move fast. When you own the product priced under that threshold, you are selling into the thickest, most active buyer pool.

This is why “flat market” headlines don’t scare me. If demand exists and you control the right product at the right price, you’re not begging for buyers. You’re letting the market do what it already wants to do: absorb good inventory quickly.

The practical way to identify the breakpoint is to combine data and reality. You look at listing counts, new listings, pending activity, and how quickly things are going under contract. Pending data is powerful because it’s current—it’s showing you what buyers are agreeing to right now. Sold data can lag or be harder to access, but pending is fresh.

When you look at a market and see a strong percentage of listings going pending, that tells you demand is real. Then you look at the properties going pending and ask a simple question: what price band is moving?

In one example, you can see a market where the “reset” is obvious—prices may have dipped compared to the peak, but they’re still moving in a predictable range. You’ll notice that the properties that go under contract quickly often cluster around a certain price point. That cluster is your clue. It’s telling you what buyers are comfortable paying. And if you want to sell quickly, you want to own something priced below that cluster.

This is where people overcomplicate the conversation by talking about condition. In a demand-heavy market, condition matters less than math—because the discount is what creates the opportunity. That doesn’t mean you ignore obvious problems that make something unsellable. It means you stop letting perfection be the requirement. You’re not trying to buy the dream house. You’re trying to control an asset that is priced right for the demand curve.

When I say “control,” I mean you have a position that lets you profit from the asset. There are multiple ways to do that in real estate, but the cleanest is simply buying it. Cash if you have it. And if you don’t have it, you partner with someone who does. In our world, this is normal. There’s capital everywhere for solid deals, and I often prefer being one of a couple partners rather than doing everything alone.

Once you know your market, know your breakpoint, and know your buy number, the rest becomes execution. You build a pipeline. You send offers consistently. You create deal flow. And you focus on velocity.

Velocity is the piece most people don’t think about. We’re not in the business of buying something and sitting on it for years hoping the market eventually rescues us. We’re in the business of moving money. Turning capital. Recycling it again and again. Because the same chunk of money used multiple times in a year can outperform a “big win” that takes forever.

That’s what the 2026 strategy looks like in plain English:

You don’t need the entire market to go up. You need a high-demand pocket, a clear breakpoint, and an asset priced below it. Then you let demand do what it does best.

While everyone else is staring at headlines, we’re staring at math.

Take a moment this weekend to connect with a fellow investor, join a discussion in our community, or dive into a new podcast episode.

If you’re ready to join these members and call yourself a successful investor in the next 60 days, join us now.

You are not alone in your real estate ambition.